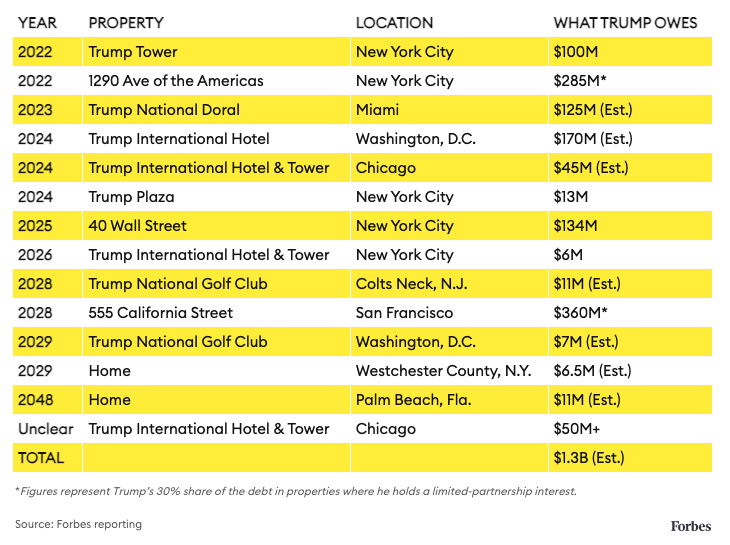

The real estate mogul should have no problem paying back his loans in the short term. But come 2024, when he might be running for president again, things could get dicey. Donald Trump’s business owes an estimated $1.3 billion, nearly $200 million more than it did when he left office. But that doesn’t mean that he’s under more financial pressure. In fact, Trump’s balance sheet is in better shape today than it was months ago.

The reason: Earlier this year, JPMorgan Chase helped loan $1.2 billion against a San Francisco office complex in which Trump holds a 30% minority interest. As a limited partner, Trump would not be personally liable for that debt in the event of a default. But it still has a huge effect on his finances. In fact, the new loan allowed Trump and his business partner, publicly traded Vornado Realty Trust, to pay back their previous debt against the building, which was due last month, and extract about $616 million in cash.

In other words, the refinancing increased the debt on the property but also provided its owners with more liquidity. If Trump received 30% of the cash out, the deal would have boosted his liquid holdings from an estimated $110 million to nearly $300 million.

That cash could come in handy over the next couple of years. In September 2022, Trump has another loan coming due, this one worth $100 million on property he owns outright—the commercial space inside Trump Tower. Theoretically, Trump could refinance that loan as well. The real estate is worth an estimated $275 million, so a bank should be willing to offer a fresh $100 million against it. Even if the former president can’t find a firm to refinance Trump Tower, he should be able to pay the money back with his own funds.

THE TIMELINE

Trump has an estimated $738 million of debt coming due over the next three years. If he is careful, he should be able to work his way through it.

He’d still probably be able to replenish his cash pile. Two months after the Trump Tower loan comes due, another piece of debt will mature—this one tied to a New York City skyscraper named 1290 Avenue of the Americas. Like the San Francisco building, Trump owns a 30% limited-partnership interest in 1290 Avenue of the Americas alongside Vornado, which holds the other 70%. If Vornado refinances that building, too, Trump could easily extract another $75 million.

Doing so would provide the former president with some additional breathing room heading into 2023, when he has two loans with a combined original principal of $125 million coming due against Trump Doral, a golf resort in Miami. That property has struggled recently, so it could be challenging to refinance. Same goes for Trump’s hotels in D.C. and Chicago, which have an estimated $215 million of Deutsche Bank debt expiring in 2024.

Put it another way: The more cash Trump can stockpile now, the safer he’ll be then—even if that means increasing his debt load in the meantime.

Source: https://www.forbes.com/sites/